Life Insurance: Secure Your Family's Future Today [Guide]

Have you truly considered the 'what ifs' that life throws our way? Ignoring life insurance is akin to leaving your family financially vulnerable; it's a crucial safety net, and understanding its nuances can be the most responsible decision you make.

Navigating the world of life insurance can initially feel like deciphering a complex code, yet the underlying principle is remarkably simple: to provide a financial shield for your loved ones when you are no longer there. This safety net is designed to alleviate the potential financial burden resulting from your passing. What complicates matters, however, is the array of policy types available, each tailored to different needs and stages of life. Term life insurance, for instance, offers coverage for a specified duration, be it 10, 20, or 30 years, providing a safety net during critical phases like raising a family or paying off a mortgage. Conversely, permanent life insurance, encompassing options like whole life and universal life, provides lifelong protection while also accumulating cash value over time, essentially serving as both an insurance policy and a savings vehicle.

| Information | Details |

|---|---|

| Concept | Life insurance is a contract between an insurer and a policyholder. In exchange for premium payments, the insurer provides a lump-sum payment, known as a death benefit, to beneficiaries upon the insured's death. |

| Purpose | The primary purpose of life insurance is to provide financial security to the policyholder's dependents or beneficiaries after their death. This can help cover funeral expenses, outstanding debts, living expenses, education costs, and more. |

| Types of Life Insurance |

|

| Key Features of Policies |

|

| Factors Affecting Premiums |

|

| Considerations When Choosing a Policy |

|

| Tax Implications |

|

| Resources | For more information and guidance on life insurance, consider consulting with a financial advisor or visiting the website of the Insurance Information Institute: www.iii.org. |

Let's embark on a more detailed exploration of the various types of life insurance policies, carefully comparing their distinct features. Understanding these nuances is key to making an informed decision that aligns with your specific needs and financial aspirations.

- Lays Peace Alles Ber Den Star Amp Die Erotikplattformen

- Erstaunlich Wie Justin Nunleys Aufstieg Beweist Onlineerfolg Ist Mglich

| Policy Type | Description | Key Features | Suitable For |

|---|---|---|---|

| Term Life Insurance | Provides coverage for a specific period (term), such as 10, 20, or 30 years. |

| Individuals seeking affordable, temporary coverage, such as those with young children or significant debts. |

| Whole Life Insurance | Permanent life insurance providing coverage for the insured's entire life. |

| Individuals seeking lifelong protection and a savings component, often used for final expenses or estate planning. |

| Universal Life Insurance | Permanent life insurance offering flexibility in premiums and death benefit. |

| Individuals seeking flexibility in their coverage and the ability to adjust premiums and death benefits as their needs change. |

For many individuals embarking on this journey, the logical first step involves consulting with a trusted life insurance provider. Numerous companies extend the courtesy of free quotes, allowing you to gain a comprehensive understanding of the associated costs and the spectrum of coverage options at your disposal. These initial consultations prove invaluable in facilitating a comparative analysis of different offerings, ultimately guiding you toward a policy that harmonizes with your specific financial objectives and personal circumstances. AAA Life, for example, presents a diverse array of life insurance solutions, spanning term, whole, and universal life insurance. To obtain a complimentary quote and personalized assistance, you can readily connect with their team of seasoned life insurance agents.

Traditional term life insurance, often exemplified by the offerings of AAA Life, stands out as a compelling choice for individuals and families in pursuit of customizable and affordable coverage, meticulously designed to safeguard their financial future. The adaptability of this coverage is a significant advantage, as it can be finely tuned to align with your unique requirements, ensuring that the death benefit is sufficiently substantial to address outstanding debts, provide crucial income replacement, and fulfill other pressing financial obligations.

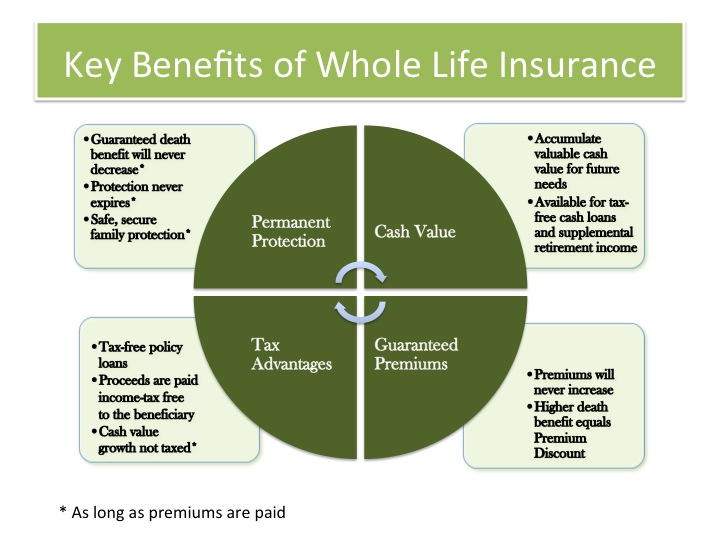

In contrast, whole life insurance distinguishes itself as a permanent policy, extending its protective umbrella over your entire lifetime. Whole life insurance is a permanent life insurance product that offers level premiums and builds a cash accumulation value. Characterized by level premiums and the accumulation of cash value, this type of policy guarantees a death benefit while concurrently fostering a tax-deferred savings component. The cash value appreciates steadily over time, presenting a valuable savings mechanism that can be accessed during the policyholder's lifetime. As a permanent life insurance policy, whole life can last until the age of 100, and you know that when you die, your beneficiaries will receive a guaranteed cash payout. Perhaps one of its most appealing attributes is the stability of premiums, which remain constant throughout the policy's duration, affording policyholders a sense of predictability and financial security.

- Ist Mkvmoviespoint Legal Ein Umfassender Blick Alternativen

- Achtung Ist Kostenlos Wirklich Sicher Der Ultimative Guide Zum Legalen Moviedownloads

With coverage ranging from $30,000 to $75,000, a whole life policy can assist with final expenses and debts, supplement a term life insurance policy, and provide additional income. Offering coverage that spans from $30,000 to $75,000, a whole life policy can serve as a versatile financial tool, providing assistance with final expenses and debts, supplementing existing term life insurance coverage, and generating additional income. In essence, it provides an added layer of protection, shielding your family from undue financial strain during times of bereavement.

AAA Life's universal life insurance policy is meticulously engineered for adaptability. Designed to endure for a lifetime, these policies offer a spectrum of options, encompassing level or flexible premiums, cash value accumulation features, and the potential to bequeath an inheritance. This empowers you with the assurance that you are actively securing your family's financial well-being, both in the present and in the years to come. Echoing the essence of whole life policies, permanent life insurance options, such as whole and universal policies, offer lifelong coverage. Moreover, premiums typically remain consistent throughout the policy's lifespan, affording policyholders stability and predictability. The guaranteed death benefit remains steadfast, irrespective of when the policyholder passes away.

The decision between term and permanent life insurance hinges on a careful assessment of your individual needs and overall financial landscape. It necessitates a thorough evaluation of your current financial responsibilities, long-term goals, and risk tolerance. If you bear the responsibility of dependents, a mortgage, or other substantial financial obligations, securing life insurance coverage becomes an indispensable element of responsible financial planning.

The policy's details matter, too. The fine print includes critical information such as riders and policy limitations. A triple indemnity rider, for example, increases the death benefit in case of accidental death. Even the minutiae of a policy warrant meticulous scrutiny. The fine print encapsulates vital information, including riders and policy limitations, which can significantly impact the policy's functionality. For instance, a triple indemnity rider can augment the death benefit in the event of accidental death, providing an extra layer of financial security. However, it is imperative to grasp the inherent limitations of such riders. As an illustrative example, the triple indemnity rider would not apply if the insured's actions contributed to their demise, as exemplified by the hypothetical case of "M," who tragically lost his life in a car accident deemed to be his fault.

When selecting a life insurance policy, also consider the financial strength and reputation of the insurance company. When embarking on the selection process for a life insurance policy, it is crucial to take into account the financial soundness and reputation of the insurance company. Opting for a provider with a proven track record of stability and exceptional customer service is paramount. AAA Life Insurance Company, holding licenses in all states except New York, serves as a prime example. Furthermore, remember to meticulously review the policy's specifics, comprehensively understand your coverage, and ascertain that the policy is ideally tailored to your unique needs and circumstances.

One product is the Guaranteed issue whole life insurance policy form series. One noteworthy product is the Guaranteed Issue Whole Life Insurance policy form series, subject to specific age requirements and policy limit restrictions. This particular policy is classified as graded benefit whole life insurance. Alternatively, exploring the option of a whole life insurance policy presents another viable avenue. While studies reveal that over 50% of individuals aged 65 and above report possessing some form of life insurance, it is imperative to recognize that life insurance policies are not uniform in their features and benefits.

There is a difference between whole life insurance and term life insurance. While a clear distinction exists between whole life insurance and term life insurance, it is important to note that term policies can evolve to accommodate changing needs. In many instances, individuals retain the flexibility to convert an existing term policy into a permanent life insurance policy if they so choose.

There is a difference between whole life insurance and term life insurance. While a clear distinction exists between whole life insurance and term life insurance, it is important to note that term policies can evolve to accommodate changing needs. In many instances, individuals retain the flexibility to convert an existing term policy into a permanent life insurance policy if they so choose. It is worthwhile to explore the compelling reasons why AAA Life stands out as an exceptional choice for term life insurance. The cash value component, an integral facet of permanent life insurance policies, such as whole life and universal life insurance, represents the portion of the policy that accrues savings over time. This savings component distinguishes these permanent policies from term life insurance, which lacks a cash value element.

AAA Life insurance policies provide financial protection when needed most. AAA Life insurance policies are meticulously designed to furnish financial protection precisely when it is most critical. To ascertain the optimal coverage options for your family's unique requirements and to obtain a complimentary online quote, we invite you to explore the available resources. Rest assured that premiums for these permanent policies will remain constant, providing financial stability and predictability.

Key Considerations When Choosing Life Insurance:

- Coverage Amount: How much life insurance do you need? The amount should cover your debts, provide for your family's living expenses, and any future financial goals.

- Type of Policy: Will term life or permanent life insurance, such as whole life or universal life, best fit your needs and budget?

- Policy Features: Consider features like cash value, riders, and dividend options.

- Company Reputation: Research the financial strength and customer service of the insurance company.

- Policy Costs: Compare premiums, but consider the long-term value and benefits of the policy.

The nuances of life insurance are best understood by a professional.Navigating the intricacies of life insurance is best accomplished with the guidance of a seasoned professional. Seeking counsel from a financial advisor or insurance agent empowers you to identify the most suitable policy tailored to your specific needs and objectives. These experts possess the requisite knowledge and experience to navigate the complexities of the insurance landscape, ensuring that you select a policy that provides optimal protection for your loved ones, thereby securing their financial well-being in the face of unforeseen circumstances. We cordially invite you to contact AAA Life today to secure your complimentary quote and embark on the journey toward comprehensive financial security.

With careful consideration and informed choices, you can find a life insurance policy that provides peace of mind and the financial security your family deserves. With careful consideration and informed choices, you can find a life insurance policy that provides peace of mind and the financial security your family deserves.

- Mehr Als Nur Eine Ehefrau Die Faszinierende Lauren Deleo Einblick

- Erome Im Visier Freiheit Oder Ausbeutung Eine Analyse

Articles Junction Types of Life Insurance Policies Life Insurance Definition Meaning

Triple A Full Coverage Insurance Life Insurance Quotes

Whole Life Insurance permanent and guaranteed protection